Kampala Student Housing: Private and Instiutional Supply, Demand & Investment Opportunities

- Market Snapshot: Student Housing in Kampala

- Demand Drivers of Kampala Student Housing: Institutions and Demographics

- Supply Landscape: From Informal Rooms to Institutional PBSA

- Key Submarkets and Neighborhoods

- Rent and Occupancy Evidence

- Outlook (12–36 Months) and Strategic Risks

- Kampala Student Housing Investment Opportunities (2026–2029)

Market Snapshot: Student Housing in Kampala

Kampala student housing remains dominated by small private hostels clustered around major institutions of higher learning. Despite the status quo, major readjustments and transformations are underway. More structured and purpose-built options are emerging. This is driven by steady demand from the city’s highly regarded universities. Despite the status quo, major readjustments and transformations are underway. More structured and purpose-built options are emerging. This is driven by steady demand from the city’s highly regarded universities.

The supply gap is most visible at Makerere University, where nine halls accommodate roughly 4,400 students. This is roughly 10% of the undergraduate population. Kyambogo University is worse off, as it can only accommodate 1,400 of its 33,400 student population, which is less than 5%.

Proposition to the Investor

Demand for rental housing in Kampala Central Business District remains reliable because it is tied to education rather than lifestyle preferences. For investors evaluating Kampala student housing, this creates a more resilient rental segment compared with traditional residential investments. This differs from the volatility seen in high-end apartments when expatriates leave or companies cut back. Recent Knight Frank reviews show prime residential occupancy holding steady at around 83%, providing an opportunity to recoup investments faster.

What’s Investable?

Kampala’s student housing market breaks down into three practical plays:

- Purpose-Built Student Accommodation (PBSA). These are modern, high-quality blocks that offer all-inclusive amenities. Makazi Hostels and Aga Khan University hostels have set the pace for investors to incorporate greater value addition in student accommodation. Students are now willing to pay a premium for functional amenities like high-speed Wi-Fi, 24/7 security, and backup power instead of simply being near campus. It is a new concept in Kampala and is attracting increasing attention.

- Public-Private Partnerships (PPPs). These are large-scale development projects backed by the government or an institution on land offered by the government or the institution. Kyambogo’s PPP Student Housing Project, to be done in phases under the Design, Build, Finance, Operate and Maintain (DBFOM) model, is an example.

- Mid-Market Conversions. Converting sections of commercial buildings could be a worthwhile investment. Investors have the option to buy existing properties for conversion and refurbishment into reliable private university student hostels. The mixed-use building trend is already well established in Kampala. Makerere University handed over Lumumba and Mary Stuart Halls to NEC Construction Works Uganda Ltd, a government agency, for renovation in a bid to address housing challenges. Investors can buy older hostels and fix them up by ensuring that they are secure and have better amenities. By implementing better management, they capture students who want more than a bare-bones room but cannot afford premium prices.

The Challenges

Despite its structural demand drivers, the sector faces several operational and regulatory challenges.

- The Building Control Act 2013 introduced stricter rules on construction standards and penalties for shortcuts. While this protects the market, it increases the compliance burden for developers.

- Uganda’s land tenure system, particularly the Mailo Land System common in Kampala, can be very complex. The dual-ownership structure can complicate the process of securing financing or selling the asset. It is better to stick to clean freehold or leasehold titles to ensure liquidity and easier access to credit.

- New supply from PPPs, like the project at Kyambogo University, could start easing shortages in a few years. This might squeeze returns if you overpay for land right now. The UNHS household data shows that incomes are tight for many families, so rent hikes beyond inflation can backfire outside niche premium spots.

- Infrastructure across the capital is not uniform. The KCCA report indicates that 35.5% of the 2020-2025 infrastructure plan was achieved. Costs for water and power outages should be factored into budgeting.

Demand Drivers of Kampala Student Housing: Institutions and Demographics

Kampala’s student housing demand is anchored by a simple fact: it is the primary education hub for both Uganda and the wider region. With over 50 licensed universities, according to the National Council for Higher Education (NCHE), the city hosts a massive, repeatable concentration of tenants. While public institutions were built for the modest student bodies of the 1960s, they now face a “youth bulge” that has pushed demand into the private sector. This cluster is stronger than the national average because it creates a high-density, predictable market.

Higher education enrolment in Uganda has experienced a steady upward trajectory over the last 15 years, growing by approximately 59% since the 2011/12 academic year. Starting from 198,066 students, the population has expanded at an average annual rate of 4.5%, officially crossing the 300,000-student milestone during the 2024/25 period. According to current projections, this growth is set to reach a record high of 315,000 students in the 2025/26 cycle, highlighting a consistent and significant expansion in demand for university and tertiary education across the country.

In Kampala, the market is dominated by two giant public institutions that set the pace for demand.

- Makerere University. As one of the oldest universities in East Africa and the flagship institution in Uganda, Makerere’s enrolment remains in the tens of thousands. The overspill of first-year undergraduate students and continuing students who cannot get accommodation in campus halls creates massive demand in areas like Wandegeya, Kikoni, and Makerere-Kivulu.

- Kyambogo University: Data from the recent admissions cycle reveals that over 2,600 students were unable to secure spots in on-campus hostels. Due to their proximity to the university, most of these students sought housing in private hostels in the Banda and Kireka areas.

- Private universities like Kampala International University (KIU) and the International University of East Africa (IUEA) attract a significant portion of regional students, adding another layer of housing demand. These institutions typically have lower ratios of on-campus beds to students compared with public institutions. Historically, the surrounding neighborhoods of Kansanga and Kabalagala have been prime territory for private rentals.

Demographic Momentum

Uganda has one of the youngest populations in the world. The 2024 National Census reported a population of 45.9 million, with half the country under the age of 18 and a median age of just 15.9 years. After completing secondary education in remote areas across the country, this demographic “youth bulge” relocates to the capital in search of tertiary education.

From the outset, public universities were not built to house every student. In addition, these institutions are not building new accommodation fast enough to keep up with their admissions. The gap between enrolment and university-owned beds remains structural. This gap is currently being filled by informal room rentals and converted residential buildings around these institutions. In most cases, these facilities lack the security and reliability that modern students are starting to demand.

The Regional Factor

As an education hub in the East African British Protectorate during the colonial period, Kampala remains a regional magnet. Its reputation for quality education and the harmonization of fees across the East African Community has attracted international students from Kenya, Tanzania, Rwanda, Burundi, DR. Congo, and South Sudan, with an approximate figure of about 16,000 international students concentrated in Kampala. This population plays major economic significance in the city.

Having travelled far from their homes and lacking local family networks, they represent ‘guaranteed’ demand for private housing. They also tend to prioritize security, stable power, and high-speed internet. This preference is what makes the Purpose-Built Student Accommodation (PBSA) model viable, as they are willing to pay a premium for a managed, ‘western-style’ living experience.

The Academic Cycle

Cash flow in this market follows the bi-semester cycle set by the Ministry of Education.

- Semester I: Runs from August to December and is the peak period for occupancy as a large volume of new students enter the market simultaneously.

- Semester II: Typically begins in January/February and ends in May.

- Recess Gap: Public universities often go on recess from June to August. Private universities have their Semester III.

To handle the June-to-August gap, some operators are moving away from semester-only deals. They are starting to use 12-month contracts or target short-term tenants like interns to keep cash flowing during this break. Investors targeting private university students stand to benefit from year-round occupancy, as these institutions run a third semester.

Supply Landscape: From Informal Rooms to Institutional PBSA

The Kampala student housing market is highly fragmented. While the city’s universities anchor demand, they provide only a tiny fraction of the housing. While the city’s universities anchor demand, they provide only a tiny fraction of the housing. This has left the private sector to fill the gap with a mix of basic rentals, mid-tier hostels, and an emerging class of professional Purpose-Built Student Accommodation (PBSA).

Institutional Supply: The Constrained Core

On-campus housing is the cheapest option. Most of these public university facilities and infrastructure date back to the colonial era. Overcrowding and inadequate maintenance have led to persistent issues such as poor sanitation and frequent power outages. This has forced the vast majority of students to find off-campus alternatives, creating a massive captive market for private developers. Public institutional hall prices serve as a price floor for the market but do not compete with the private sector on quality or availability.

Private Hostels: The Grade-Based Market

Private hostels are the real backbone of market supply. In addition to protecting students, Makerere University actually accredits these private hostels through an annual inspection committee, grading them from A (Excellent) to C (Good), based on safety and the availability of amenities.

Most of these hostels are owned by small landlords and operate at capacities of 50 to 200 beds. The “Grade A” label is a major marketing tool, allowing landlords to command higher rents because they guarantee basic amenities like 24/7 security and Wi-Fi.

Strategic Submarkets: The “Campus Towns”

The performance of Kampala student housing varies significantly by submarket, with proximity to universities remaining the biggest driver of occupancy and rental premiums. Several neighborhoods around major universities have evolved into dense student housing submarkets. In the capital, the student sub-market is grouped into three neighborhoods and is concentrated around the Makerere-Kyambogo corridor.

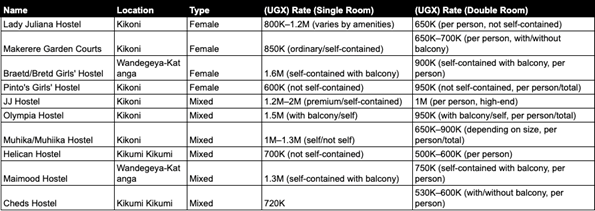

- Kikoni: Considered the heart of Makerere’s student life. It is characterized by a high student population density, many large student hostels, and affordable markets and food stalls. Double rooms here go for UGX 1.1M to 1.7M per semester (Market triangulation of 2025/26 listings from Private Property Uganda and Jiji (Q1 2026)).

- Wandegeya: More commercial and upscale. With a solid population, a number of supermarkets, restaurants, and recreational facilities, the area has a 24-hour economy. Rents are higher, with a single room in this hub reaching UGX 1.7M per semester because of enhanced security, 24/7 access to shops, and transport.

- Banda/Kyambogo: This area serves Kyambogo University. It’s generally more affordable but suffers from poor roads and water issues. This creates an opportunity for developers able to deliver higher-quality accommodation.

Price Ranges per semester (approx. 4 months) for Private Hostels in Wandegeya, Kikumi Kikumi, and Kikoni (Sources: Private Hostels Makerere, Campus Bee Hostels Review, Makerere University – Student Housing Portal, Knight Frank – Kampala Property Market Review H2 2025)

Current Supply Metrics (2025/26, sources: Private Hostels Makerere; UTAMU Hostels Options; MUST Hostels; Campus Bee Hostels Review)

The Rise of PBSA

Purpose-Built Student Accommodation (PBSA) is becoming one of the fastest-growing segments within Kampala student housing, especially among international and postgraduate students. Purpose-Built Student Accommodation (PBSA) is the segment every serious investor is watching. The proposed Kyambogo University PPP Student Housing Complex will feature 12 multipurpose residential block halls with a – questionable – total, 10,000-bed capacity and amenities such as a food court, churches, parking, a restaurant, a gym, and a spa. The 20-acre piece of land set aside by the university is meant for building modern blocks with shared kitchens, full amenities, and professional management.

A similar concept is popping up in Nakawa and Makindye to serve large numbers of businesses and students. In 2025, two major hostels made headlines in the area. The ongoing 540-bed capacity Makazi Hostels, developed by CrossBoundary Real Estate, is proof of attractive prospects for investors. The new 97-bed capacity Aga Khan University hostel charges UGX 4.64M and UGX 2.32M for single and double rooms respectively. Students are willing to pay higher rents to access additional services and quality amenities.

The Utility Premium

Reliable electricity is no longer a luxury but a necessity for students in Kampala. According to UBOS, while only 25% of households nationwide are connected to the national grid, Kampala enjoys higher coverage of 55%. Despite this, persistent blackouts remain common in the capital, allowing hostels that offer solar backup or generators to command significantly higher rental premiums.

Investor Takeaway

Simply put, Kampala’s supply is static at the bottom (college accommodation halls) and messy in the middle (informal hostels). Growth is at the top. If an investor treats this as an operating business by focusing on quality housing, reliable utilities, and professional management, they can capture the “flight to quality” that is currently defining the 2026 market.

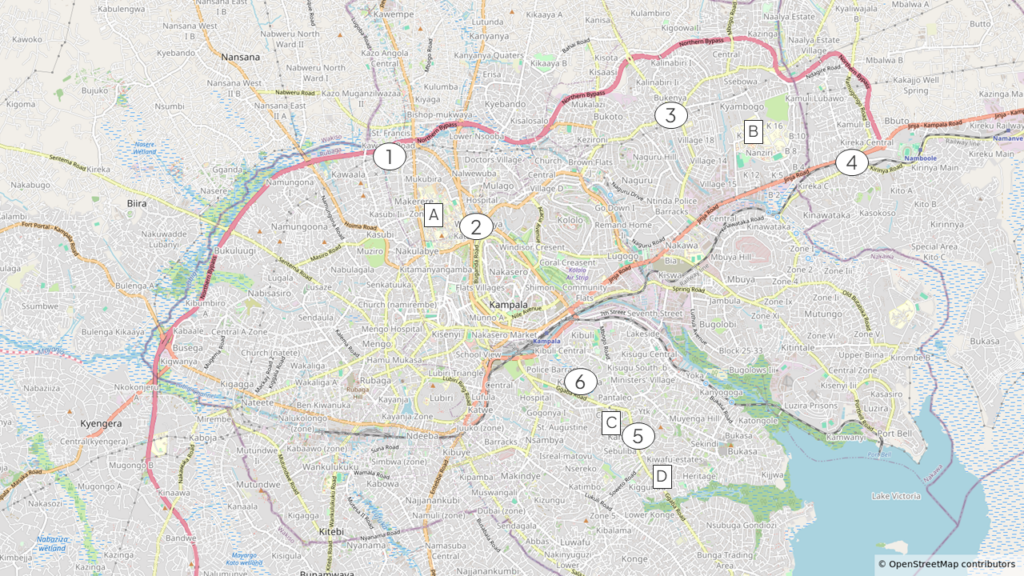

Key Submarkets and Neighborhoods

Students in Kampala prefer neighborhoods based on proximity to campus, safety, and whether utilities like power and water actually work. Because traffic and transport availability can be unpredictable, most students stick to tight clusters around the major universities. They look for accommodation within a 15-minute walk or a very short boda-boda ride. Most students – as long as they can afford it – are ready to pay a premium to get accommodation within a close radius of the universities.

The Makerere Hill Cluster: Kikoni (1) and Wandegeya (2)

This is the most established student zone in the city serving Makerere University Main Campus [A].

- Kikoni sits right at the base of the hill and functions as a classic “student village.” Many hostels here are a 5 to 15-minute walk to the main gates.

- Wandegeya is the busier neighborhood. It’s packed with shops and restaurants, which makes it great for convenience but much noisier.

The constant foot traffic provides some natural surveillance, hence moderate safety. Students prefer gated compounds that come with 24/7 security. The Makerere Hostel Inspection Committee (HIC) grades accredited hostels from A (Excellent) to C (Good) based on annual reviews. Grade A options like Olympia, New Nana, and Lady Juliana are the gold standard because they emphasize the security features that justify their higher price tags.

Utilities are a constant battle in this cluster. Hostels with higher value addition in terms of sanitation and security charge rents as high as double the average price level.

The Kyambogo Cluster: Ntinda (3) and Kireka (4)

Most students from Kyambogo University [B] live between Ntinda and Kireka, both within easy walking distance to the college. Even though the roads are not congested, the infrastructure can feel a bit rougher.

In this cluster, the biggest challenge is that hostel rooms are not self-contained, and many off-campus hostels still rely on shared bathrooms. Landlords who have added modern en-suite units in Banda are witnessing immediate demand from students who want privacy over the old dormitory-style setups.

The Southern Cluster: Kansanga (5) and Kabalagala (6)

This area serves Kampala International University (KIU) [C] and the International University of East Africa (IUEA) [D]. It has a more international feel, with high-end supermarkets and shopping malls. The 24-hour economy vibe adds to the sophistication, appealing to local students and, especially, the large international population.

Since campuses are more spread out in this cluster, students usually have to choose between longer walking time, busses (taxis) or boda-bodas for transportation. Utilities are there, but they are better in the newer buildings. Because international students often stay through the holidays, this is one of the few spots where 12-month leases are actually viable. It is a particularly suitable area for premium PBSA.

Cross-Cluster Observations (Premiums estimated from Q1 2026 listing analysis across 60 properties in three clusters.)

Investor Takeaway

Since location is the first filter in real estate investment, an investor is expected to be in the “gold zones” within 15 minutes of the campus gates if they want the strongest fill rates. That is why Kikoni and Wandegeya command the highest rents due to their walkable proximity to Makerere University.

Utilities are the second filter. A well-positioned property will still struggle if it doesn’t have security, water tanks, and backup power. Investors should budget for hybrid solar from the start and make sure they comply with the regulatory framework, which has raised the bar for construction permits and safety standards. This is because students look for study-friendly environments when seeking accommodation.

Rent and Occupancy Evidence

Rent performance in Kampala student housing follows predictable semester-based demand cycles. Student housing in Kampala runs on semester cycles. The semester leasing structure allows operators to collect rents upfront. This supports strong cash-flow cycles despite recess periods, which require careful planning to avoid revenue gaps.

The Pricing Floor: On-campus Halls

University halls anchor the low end of market rates. Makerere charges private students about UGX 330,000 to 350,000 per semester for a bed. These are basic shared rooms with communal facilities. With limited beds available, only government-sponsored first-year students are offered on-campus accommodation. The rest are pushed toward private rentals.

Private Market Benchmarks (2025/26 Academic Year)

Rents depend on room density. The more students share a room, the lower the price per person. These figures are based on analysis of 30 listings from Private Property Uganda and Jiji (Q1 2026), cross-referenced with Makerere’s accredited hostel list.

Note: Prices are per student, per semester.

Estimated 2025/26 Semester Rent by Submarket (Sources: Private Hostels Makerere; UTAMU Hostels Options; MUST Hostels; Campus Bee Hostels Review)

These are asking prices, so actual deals can fall 5% to 10% lower after negotiation. Kikoni and Wandegeya command a premium for being within walking distance of Makerere, while Nakawa trends higher because of newer builds near the business school (MUBS).

Occupancy and the Recess Gap

The chronic bed shortage keeps occupancy high. Grade A hostels in Wandegeya, Kikoni, and Nakawa are at full capacity during campus sessions. Broader residential occupancy in prime areas sits at about 83%. Student properties in campus clusters hold much firmer because demand is not optional.

The June to August recess gap is the main risk for investors’ cash flow. Successful operators counter this by offering 12-month leases (which are popular with international students in Kansanga) or by using the break for short-term lets to interns, researchers, and visiting professionals.

Investor Takeaway

For student housing investment in Kampala, location drives occupancy. The Nakawa area near MUBS currently offers the best balance. It has higher-budget students, consistent demand, and plenty of room for property upgrades. Utilities drive rent. Reliable generators, water storage, and en-suite bathrooms justify the premiums required for a strong net yield.

Outlook (12–36 Months) and Strategic Risks

Kampala student housing is moving into a phase of professionalization. While private low-cost options dominate the market, the next three years will reward investors who focus on operational quality rather than simply adding more beds. While private low-cost options dominate the market, the next three years will reward investors who focus on operational quality rather than just adding more beds.

What Supports the Narrative

UBOS reports show that the under-18 population, which accounts for half of the country’s total population, will ensure a steady flow of students into the tertiary system through 2028. This demand is essentially non-discretionary. Most institutions are shifting strategy to meet market demand. Makerere University is aiming for a 30% increase in postgraduate enrolment by 2030 while simultaneously cutting back undergraduate intake. This is a major signal for the market because postgraduates generally have higher budgets and much lower tolerance for the “informal” hostel experience. This shift directly supports the case for Purpose-Built Student Accommodation (PBSA).

On the macro side, conditions are relatively stable. The Bank of Uganda held the Central Bank Rate at 9.75%. With inflation projected between 3.8% and 4.3% for FY2025/26, living costs remain manageable for middle-class families, supporting their ability to pay for ‘Grade A’ housing.

Investment Risks

- The most significant risk is the upcoming supply “shock.” Even a partial delivery of 2,500 beds by the Kyambogo University PPP project across 12 blocks within a three-year period could cap rent growth in the Banda and Kireka submarkets. Similar pipelines may emerge at the Business School (MUBS) and other regional universities, which aim to add 15,500 beds in total over the medium term.

- Economic growth is also being recalibrated. Despite a projected 10.4% growth rate, in January/February the Ministry of Finance recently lowered its 2026/27 GDP growth forecast to between 6.5% and 7%. While still robust, it suggests that the “oil boom” will be a gradual climb rather than an overnight lift in urban incomes.

- The complex Mailo land system deters prospective investors because of the high cost of acquiring construction land. Overlapping claims make banks cautious about using student housing as collateral, which keeps the cost of private capital high. This favors investors with strong equity positions or those who can secure clean freehold titles.

Investor Implications (2026–2029)

The “High-Yield Corridor” of Makerere Hill, Nakawa, and Kansanga offers the strongest resilience. These zones attract international and postgraduate students who are least affected by the new government-backed “standard” beds. These tenants are most willing to pay a premium for reliable power, water, security, and internet.

Kampala Student Housing Investment Opportunities (2026–2029)

Kampala’s student housing market is no longer a simple land bet. To make it work, an investor must treat it as a professional operating business. While the structural undersupply and non-cyclical demand are strong foundations, actual returns will come down to location, utility reliability, and the investor’s ability to deliver a better experience.

Core Opportunities for 2026–2029

- Mid-tier Upgrades in Established Clusters: Target older hostels in Kikoni, Wandegeya, Banda, or Kireka. These properties serve the massive base of local students who prioritize affordability and proximity, so entry costs will be lower compared with new construction. Private hostels are at full occupancy during session, forcing some students to opt for informal settlements.

- Premium PBSA in the Southern Zone: Focus on Kansanga and Kabalagala near KIU and IUEA. These areas attract international and private-university students willing to pay UGX 2.5M to 4M+ per semester for en-suite rooms, 24/7 security, and high-speed internet.

- Partnering with PPPs: For instance, Kyambogo University PPP envisions a residential complex within the institution with a 10,000-bed capacity. Other similar university pilots are actively seeking private partners for financing, construction, and operations. This allows investors to build on university-owned land, eliminating land-acquisition risk while securing structured, long-term revenue.

Managing the Real-world Risks

- The Supply Shock: New beds from the Kyambogo PPP could soften rents in Banda and Kireka after 2028. If you are entering the market now, prioritize Makerere Hill and the Southern clusters. They offer more diversified tenants and face less immediate pressure from government-backed supply.

- The Land Trap: Mailo systems with overlapping claims make banks cautious about collateral and can delay projects for years. Always verify clean freehold or leasehold titles through the UgNLIS (Ministry of Lands portal) before committing any capital.

- The Recess Gap: Demand dips during the June to August break. Bridge this by offering modest discounts for 12-month commitments or by pivoting to short-term lets for researchers, interns, and visitors who flood the city during the university holidays.

Practical Steps to Get Started

When selecting a site for student accommodation development, investors should begin by following the 15-minute rule: prioritize a location within a 15-minute walking radius of the main campus gates of Makerere University or Kyambogo University. Premium opportunities can also be found in neighborhoods such as Kansanga, which are popular with students due to their proximity to universities and social amenities.

Verify market prices by sampling at least 30 current listings on property platforms such as Jiji or Lamudi to determine what students are actually paying during the current semester, rather than relying on outdated historical averages.

It is also important to budget for regulatory compliance. The recently enacted Real Estate Act 2024 requires project registration and enforces stricter safety and development standards. As a result, developers must account for these costs early in the planning phase to avoid potential fines or construction delays from the authorities.

Finally, prioritize reliable utilities and essential services that address common student concerns. In Kampala’s student accommodation market, hostels that consistently provide dependable security, adequate water storage, and stable electricity supply tend to maintain full occupancy and command the highest rental premiums.

Strategic Takeaway

The window for “easy” gains is closing as the market matures and institutional supply arrives. However, demand remains stable. A young population and limited on-campus beds ensure that the tenant pipeline stays full through the end of the decade. Investors who secure strong locations now and invest in reliable amenities will hold high-occupancy, inflation-hedged assets. In a market where thousands of “standard” beds are on the way, the real defense is delivering a superior tenant experience that public-sector projects struggle to match. For investors, Kampala student housing remains one of the strongest education-linked real estate opportunities in Uganda, supported by structural undersupply and consistent tenant demand.

By Edwin Ngoko | Edited & published by TwentyFirst Real Estate.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or real estate advice. While we strive for accuracy, data and market conditions may change. Please consult a qualified professional before making any decisions.