Student Housing Investment in Nairobi: Market Trends & Opportunities

- Market Snapshot: Student Housing In Nairobi, Kenya

- Demand-Supply Gap in Nairobi’s Student Housing Market

- Supply Landscape And Segmentation

- Key Submarkets And Neighbourhoods

- Rent And Occupancy Evidence

- Future Outlook of Nairobi Student Housing: 12 To 36 Months

- Investor Implications And Opportunities

According to the Commission for University Education (2024), Kenya recorded 628,541 students enrolled across accredited universities, with Nairobi hosting the highest concentration of public and private institutions nationally. The largest institutions in Nairobi are the University of Nairobi with approx. 41.000 students and the Kenyatta University with approx. 36.000 students. Both universities are accounting together for over 12% of the total university enrolment. The uniRank directory lists approximately 27 universities and degree-granting institutions based in Nairobi County alone, establishing the city as Kenya’s premier student hub. Student housing investment Nairobi is rapidly emerging as one of Africa’s most attractive real estate opportunities. The broader student housing Nairobi market is driven by rising university enrolment, a widening accommodation gap, and strong rental yields.

Nairobi is rapidly emerging as one of Africa’s most attractive destinations for student housing investment and real estate investment in Kenya. With rising university enrolment, a widening accommodation gap, and strong rental yields, the Nairobi student housing market offers a compelling opportunity for investors seeking stable, high-growth assets.

The housing infrastructure has not kept pace. The Ministry of Education reported available student housing Nairobi stock of 300,000 beds against a national university enrolment of 520,900 as far back as 2018—with enrolment since growing significantly and no equivalent expansion in institutional bed capacity recorded. The National Housing Corporation’s Strategic Plan 2023–2027 independently corroborates the pressure, identifying student accommodation shortage as accounting for 40 percent of Kenya’s total housing deficit.

Market Snapshot: Student Housing In Nairobi, Kenya

What is Student Housing Investment?

Student housing investment refers to acquiring or developing residential properties specifically designed for university students, offering predictable demand, recurring rental income, and strong occupancy driven by academic cycles.

Why The Market Matters

Demand that renews by design. Unlike conventional residential markets, where occupancy depends on household formation, employment migration, and broader economic sentiment, student housing demand is institutionally programmed. Each year, new cohorts are admitted, continuing students require ongoing accommodation, and graduating classes are replaced by fresh entrants. This intake-replacement cycle produces recurring demand that does not disappear during economic downturns—it may compress in affordability, but it does not evaporate. The Kenya Universities and Colleges Central Placement Service (KUCCPS) releases annual placement results ahead of each academic intake, providing visibility into incoming cohorts before the leasing season begins. That predictability is rare in real estate and is one reason student housing is recognised globally as a defensive sub-sector.

A supply gap that is widening, not closing. Public universities provide halls of residence, but available beds represent a fraction of total enrolment. According to Cytonn Research, on average, higher institutions in Kenya only cater to approximately 23% of their student population, with the remainder relying on private accommodation. This assessment corresponds to the actual situation at the University of Nairobi. The university has a total on-campus accommodation capacity of approximately 9,863 beds across eight campuses, meeting the needs of only 24% of its enrolled student population, according to the UoN PBSA Project Information Memorandum published by the PPP Directorate.

Relative attractiveness within Nairobi’s broader property market. Nairobi’s office and retail sectors have faced sustained pressure from oversupply, remote working trends, and shifting consumer behaviour. In this environment, student housing offers a bed-based revenue model that generates higher income density per square metre than unit-based residential letting, occupancy anchored to academic cycles rather than employer sentiment, and a tenant base that renews predictably. Cytonn Investments recorded student housing rental yields averaging 7.0% in 2022, up from 6.9% in 2020—outperforming conventional residential at 5.4% in FY2024/25 and broadly in line with serviced apartments at 7.3% in 2024—positioning student housing as a resilient income-generating asset class within Nairobi’s real estate market. The market’s institutional trajectory is evidenced by the performance of Acorn Investment Management’s ASA REIT, Kenya’s largest PBSA operator: according to the ASA I-REIT 2024 Annual Report, the combined portfolio stands at 21,000 beds with total assets under management of KES 26.4 billion, and the fund surpassed KES 1 billion in annual rental revenue for the first time in 2024. Learn more about real estate investment opportunities in Africa

What’s Investable

Purpose-Built Student Accommodation (PBSA). PBSA represents the most institutional-grade segment of the market. These developments are purpose-designed for students, professionally managed, and positioned within reach of major university clusters: the Parklands and Chiromo zone serving University of Nairobi’s medical and science campuses, Kilimani and Hurlingham for Strathmore and surrounding colleges and Ruaraka for USIU-Africa. Established operators such as Qwetu have built their model around serving multiple institutions simultaneously rather than anchoring to a single campus, which reduces concentration risk and improves occupancy resilience. PBSA operates on a per-bed revenue model that generates higher income density than unit-based residential letting, and formal lease structures improve cash flow predictability. The trade-off is higher capital expenditure and stronger location dependency—an asset positioned beyond practical commuting distance of at least one major institutional anchor will struggle to sustain occupancy regardless of specification.

Mid-Market Cluster Hostels. This segment serves the largest share of Nairobi’s student population: domestic undergraduates from public universities who prioritise affordability and commute time over amenities. Assets typically take the form of mid-rise blocks with shared rooms of two to four occupants, basic furnishings, shared or minimal in-room cooking facilities, and on-site security. Demand is highly location-sensitive, anchored to proximity and transport access to major public universities.

Value-Add Repositioning. A significant portion of stock near major campuses is informally managed, under-optimised for per-bed revenue, and operating without the systems or lease structures that a professional operator would introduce. Acquiring and upgrading these assets can require materially less capital than ground-up development while still capturing campus-proximity demand. The return logic is not speculative rent escalation but operational tightening: structured leases, centralised rent collection, utility reliability, and incremental specification upgrades that justify pricing above the informal market.

What’s Risky

Policy and higher-education funding. Kenya’s shift to the Higher Education Loans Board (HELB) Student Centred Funding Model, unveiled by President Ruto on 3 May 2023 and implemented from September 2023, introduced means-tested bursaries and loans intended to broaden access, but implementation has been uneven. Delays in bursary disbursement directly affect students’ ability to meet housing costs, and any further restructuring of the model—or reversion to a less targeted funding approach—would compress housing budgets across the mid-market segment, which draws predominantly from public university cohorts

Macroeconomic volatility. Kenya experienced significant currency and inflation pressure between 2022 and early 2024. The Kenyan shilling lost approximately 20 percent of its value against the US dollar over that period before partially recovering. According to the Kenya National Bureau of Statistics, inflation peaked at 9.6% in October 2022, moderated to 5.1% by May 2024, and has since stabilised further to 4.5% as at November 2025. These pressures affect the market in two directions simultaneously: tenant affordability compresses at the same time that construction input costs and financing rates rise. Notably, the ASA I-REIT 2024 Annual Report recorded an average occupancy of 87% across its portfolio in H1 2024 despite a disrupted academic calendar—suggesting that professionally managed PBSA can sustain occupancy even under macroeconomic strain, while informal and mid-market stock remains more exposed.

Micro-market oversupply. A building 300 meters from a campus gate can perform materially differently from one two kilometres away without reliable transport links. If multiple mid-market developments are delivered simultaneously within the same catchment zone—a realistic scenario along the Thika Road spine given growing developer interest—pricing competition intensifies and vacancy periods lengthen. This risk is highly localized: an influx of new supply in a single neighbourhood can trigger high vacancy and pricing pressure in that specific corridor, even while other parts of the city remain undersupplied.

Operational and management risk. Student housing is more management-intensive than conventional residential letting. Dense occupancy accelerates maintenance wear. Tenant turnover is structurally high, with leasing cycles tied to academic calendars rather than individual household decisions. Rent collection in the informal segment is often cash-based and inconsistent. Security incidents and utility interruptions—power outages and water rationing are common in peripheral estates—can damage reputation quickly in a market where word of mouth among student networks travels fast

Regulatory and compliance risk. Nairobi County has periodically signalled intent to enforce zoning, fire safety, and building compliance standards more rigorously in high-density residential areas. Informally converted hostels—buildings that have shifted from residential to student accommodation use without formal change-of-use approval—carry latent compliance exposure that can materialise suddenly. Fire safety enforcement has precedent as a trigger for forced closure or costly remediation.

Demand-Supply Gap in Nairobi’s Student Housing Market

Institutional Anchors And Campus Geography

Public university anchors. Public institutions generate the deepest and broadest demand pool, particularly for mid-market accommodation. The University of Nairobi is the most geographically complex anchor in the city, operating seven campuses across the CBD, Chiromo off Riverside Drive, Parklands, Lower Kabete, Kikuyu, Ngong Road, and Kenyatta National Hospital. The University of Nairobi managed to admit 13.000 new students in the 2024/2025 academic year. Kenyatta University, headquartered in Kahawa along the Thika Road corridor, anchors the most structurally important single student accommodation spine in Nairobi. Its scale drives sustained demand across Roysambu, Kahawa Wendani, Githurai, and Kasarani. The Technical University of Kenya, located within the CBD, reinforces demand in Ngara and Pangani.

Private university anchors. Private institutions shape the upper-mid and premium segments of the accommodation market, where tenants are less price-sensitive and more amenity-conscious. Strathmore University, located along the Madaraka and Kilimani axis, attracts a mix of domestic middle-class and regional students whose accommodation preferences support demand in Kilimani, Hurlingham, South B, and along Ngong Road. USIU-Africa, located in Ruaraka, draws both Kenyan and international students from across East Africa. Its relative geographic isolation from the CBD makes proximate accommodation in Ruaraka and along the Thika Road approach a near-necessity rather than a preference, which structurally strengthens occupancy for well-located assets in that corridor. Daystar University and a cluster of smaller private colleges further reinforce CBD-adjacent demand.

Why institutional diversity matters for investors. A market anchored to a single institution carries meaningful concentration risk—a policy change, enrolment decline, or campus relocation at one university can materially impair demand across an entire corridor. Nairobi’s multi-institutional structure distributes that risk. An asset well-positioned along the Thika Road spine draws from Kenyatta University, USIU-Africa, and several smaller colleges simultaneously. A property in Parklands serves UoN medical students, private college attendees, and students from Westlands-area institutions. This layered catchment is one of Nairobi’s most underappreciated demand characteristics and one of the stronger arguments for the market’s medium-term resilience. Explore our Kenya real estate market insights for deeper analysis

Enrolment Indicators And Intake Structure

Kenya’s public university placements are centrally coordinated through KUCCPS, which releases placement results annually before the start of each academic year.

Nairobi-based institutions consistently absorb a significant share of national placements given their concentration of high-demand programs in medicine, law, business, and engineering.

The intake follows a predictable sequence: KUCCPS releases placement results, reporting dates are issued, and students admitted from counties outside Nairobi—a substantial proportion of public university entrants—must relocate before orientation begins. This triggers a compressed leasing season in August and September where demand is concentrated and decisions are made quickly. First-year students who secure accommodation near campus tend to remain in the same corridor for the duration of their studies, creating a multi-year tenancy base that stabilises occupancy and reduces ongoing marketing intensity.

Demographics And International Students

With a median age of 20.0 years, according to World Economics, Kenya has one of the youngest population profiles globally. The practical implication is that the cohort currently moving through secondary school and into university is large, and will remain large for the foreseeable future.

According to the Commission for University Education, Kenya’s university enrolment rose 152 percent over twelve years—from 240,551 students in 2012, to 559,620 in 2022/23, to 628,541 in 2024. In 2024, CUE data shows that 577,345 students were enrolled at the undergraduate level. Master’s programmes enrolled 40,959 students. At the doctoral (PhD) level, enrolment stood at just 8,666 students. Most of the students arrive without established housing networks in the city and carry income profiles that support mid-to-premium price points, making them a structurally attractive tenant segment for PBSA operators and upper-mid market hostels in the Ruaraka and Kilimani corridors specifically.

Academic Calendar And Seasonality

Nairobi’s universities predominantly operate on trimester or semester systems, running three cycles across the academic year: September to December, January to April, and May to August. Each cycle opens with registration and orientation before moving into teaching weeks, examinations, and a short break. This calendar structure has direct implications for occupancy patterns, cash flow timing, and operational planning.

The primary leasing season runs from August through September, when first-year students arrive and the largest cohort of returning students secures or renews accommodation. This is the highest-pressure period in the market: demand is concentrated, search timelines are short, and well-located properties at competitive price points fill quickly. A secondary intake occurs in January, smaller in volume but still meaningful for operators with vacancies created by mid-year departures. Outside these two windows, demand stabilises rather than disappears—Nairobi’s year-round academic activity and the presence of continuing students mean that occupancy does not collapse between intakes the way it might in markets with a single annual cycle.

The cash flow profile of student housing in Nairobi differs from conventional residential letting in ways that matter for financial modelling. Rental payments frequently align with university fee payment deadlines rather than calendar months, producing lump-sum inflows in October, January, and May rather than evenly distributed monthly receipts. Investors accustomed to monthly residential cash flows need to model this pattern explicitly and ensure that operating cost structures—maintenance, staffing, utilities—can be managed through the periods between payment cycles without cash flow strain.

Supply Landscape And Segmentation

On-campus accommodation (Budget tier). Rooms are typically shared between two and four occupants, furnished to a basic institutional standard, with utilities bundled into semester fees and strict residency rules governing occupancy. The University of Nairobi has approved a Public-Private Partnership (PPP) to add 4,000 beds across three campuses under a 30-year Design-Build-Finance-Operate-Transfer (DBFOT) model. While feasibility studies were completed in 2024 and reported by The Star in April 2025, the current bed count remains critically insufficient. Even after integrating these 4,000 additional beds, the total on-campus accommodation would only cover approximately 34% of the current student population. Crucially, this figure does not account for the consistently rising annual enrollment, suggesting that the supply-demand gap will continue to widen unless further large-scale developments are fast-tracked.

Private cluster hostels (Budget to Mid-tier). This is the dominant supply category, capturing the largest share of student demand across all major corridors. Assets are typically converted residential blocks or purpose-built low-rise buildings with shared rooms of two to four occupants, basic furnishings, minimal or shared cooking facilities, guarded entry, and a caretaker providing on-site oversight. Management is local and informal in most cases—rent collection is often cash-based, lease agreements are loosely documented, and maintenance is reactive. This segment serves primarily domestic undergraduates from public universities and is the most accessible entry point for private capital, with average monthly pricing of approximately KES 10,467 according to Cytonn Investments.

Purpose-built student accommodation—PBSA (Mid to Premium tier). PBSA represents the formalising edge of the market. These purpose-designed developments are professionally managed, featuring tiered room configurations, fully furnished units, biometric or CCTV security, dedicated study areas, backup power and water systems, and managed fibre internet. Lease agreements are formal, typically annual, with structured pricing tiers and centralised management. Operators such as Qwetu serve multiple institutional catchments simultaneously rather than anchoring to a single campus. Achievable rents range from KES 24,000 for cluster units to KES 34,000 for premium single rooms. The trade-off for investors is higher capital expenditure and stronger location dependency.

Informal rentals (Budget tier). Informal rentals function as overflow supply, absorbing students priced out of or unable to access the segments above. These are conventional residential units—bedsitters, single rooms in shared houses—with no student-specific design, no per-bed optimisation, inconsistent maintenance, and minimal security infrastructure. Management quality varies entirely by individual landlord. The investment case, where it exists, rests on repositioning: acquiring informally let stock near campus corridors and reconfiguring it for student occupancy with professional management.

Key Submarkets And Neighbourhoods

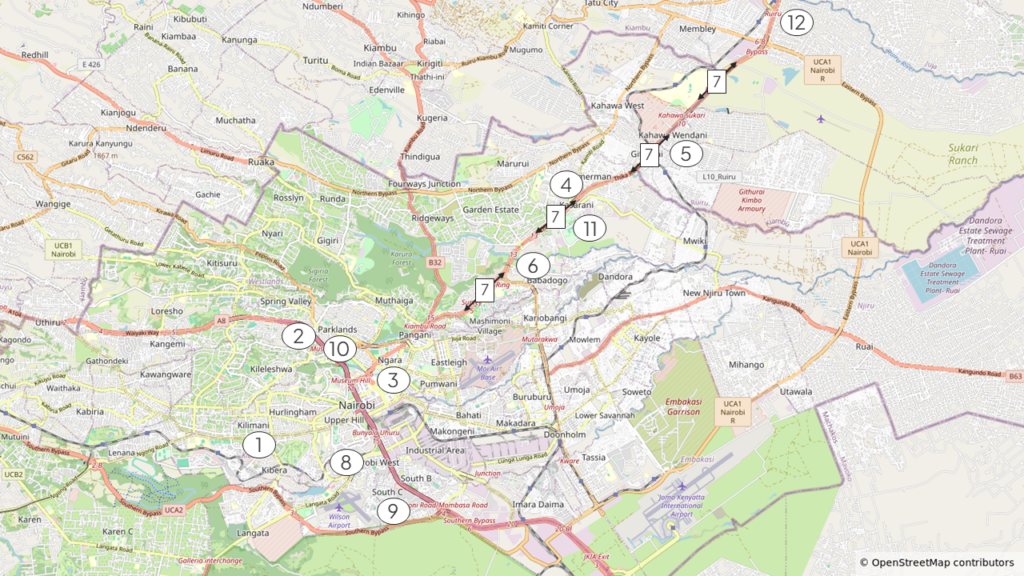

Student housing demand in Nairobi is corridor-driven rather than neighbourhood-branded. Within each corridor, performance is determined by four interacting variables: campus proximity, transport connectivity, safety perception, and utilities reliability. Power outages are a documented and recurring operational risk in key student acccommodation corridors—Kenya Power’s August 2025 maintenance notices explicitly listed Roysambu and Githurai 44 among affected areas, while Kasarani was hit by a nationwide blackout in December 2025.

Nairobi commuters spent over 26 minutes per 10 km in traffic, ranking the city among the most congested globally in 2024 according to the TomTom Traffic Index—making proximity to campus a practical necessity rather than a preference.

Kilimani (1) and Westlands (2) command premium rents because they combine stronger security perception with more reliable power, stable water supply, and high-quality fibre connectivity. In contrast, Ngara (3) and Roysambu (4) compete primarily on affordability and require active mitigation of security and perimeter control risks.

Submarkets fall into two practical categories. Core nodes—Kahawa Wendani (5) for Kenyatta University, Ruaraka (6) and Roysambu for USIU-Africa and the Thika Road (7) corridor, Madaraka (8) and South C (9) for Strathmore, and Ngara and Parklands (10) for the University of Nairobi—consistently deliver strong occupancy fundamentals. Secondary growth nodes such as Kasarani (11) and Ruiru (12) offer lower land entry points but require deliberate mitigation of utilities reliability and security perception risks to achieve comparable performance.

Rent And Occupancy Evidence

Rent levels in Nairobi’s student housing market vary significantly by segment, submarket, and room configuration. The figures below draw from verified operator listings, the HassConsult Rental Price Index—Kenya’s longest-running independent quarterly property index, covering over 320 suburbs and towns—and institutional fee schedules.

On-campus accommodation sits at the subsidised floor of the market. The University of Nairobi’s lowest reported rate is approximately KES 17,000 (130 USD) per semester, equivalent to KES 4,000 (30 USD) per month. The Co-operative University of Kenya lists accommodation at KES 12,000 (93 USD) per semester. These rates are not commercially replicable by private operators and function as a pricing baseline rather than a competitive benchmark.

Private cluster hostels occupy the budget-to-mid tier. HassConsult’s rental data places the average one-bedroom unit in Nairobi at KES 14,000 (108 USD) per month, with two-bedroom units averaging KES 40,000 (310 USD) —figures that frame the broader residential market within which student hostels compete. Student-specific shared configurations, where per-bed rather than per-unit pricing applies, typically range from KES 6,000 (46 USD) in outer corridors such as Githurai and Uthiru to KES 20,000 (155 USD) for better-specified single-occupancy units near campus in corridors such as Kahawa Wendani and Ngara.

PBSA operators achieve materially higher per-bed yields. Verified pricing from Qwetu around the USIU-Africa corridor places cluster units at approximately from KES 24,000 (185 USD) per month to KES 34,000 (263 USD) per month — the premium over mid-market hostel pricing is justified by managed utilities, security infrastructure, and formal lease structures.

Informal rentals sit at the budget floor, with bedsitters near central campuses in Ngara and Pangani ranging up to KES 12,000 (93 USD) and outer-corridor units up to KES 8,000 (62 USD). On occupancy, formal data is limited but operator and campus accommodation office feedback consistently indicates near-full utilisation during the August to December and January to April peak periods, with modest dips during inter-trimester breaks.

Future Outlook of Nairobi Student Housing: 12 To 36 Months

What strengthens the case. Kenya’s national enrolment grew 12 percent year-on-year to 628,541 in 2024, reflecting a decade-long expansion trend. The CBC cohort now progressing through secondary school represents a structurally larger pipeline entering university from approximately 2029 onwards—a timeline confirmed by both KUCCPS and the Commission for University Education—extending the demand horizon beyond the immediate window. Kenya’s student-centred funding model, introduced in 2023, initially created affordability uncertainty, but as implementation matures and bursary entitlements become better understood, housing budgets should stabilise and may actually broaden access to mid-market accommodation for lower-income cohorts. Private university expansion at institutions such as USIU-Africa and Strathmore continues to support the premium PBSA tier, where tenants are less price-sensitive. Kenya’s inflation decreased to 3.6 percent by September 2024, easing both tenant affordability constraints and investor financing costs relative to the 2022 to 2023 peak.

What breaks the thesis. The Thika Road spine is attracting growing developer interest, and simultaneous delivery of multiple mid-market projects within the same catchment zone would intensify pricing competition—a risk that is segment-specific, as new affordable developments serve genuine unmet demand rather than creating oversupply pressure. SCF implementation failure—delayed bursary disbursements, political reversal, or poor administration—would compress housing budgets across the public university segment. Financing cost volatility remains a live risk for greenfield development, where project finance is expensive and construction input costs remain sensitive to currency movements.

Nairobi’s student housing sector presents a rare combination of high demand, strong yields, and long-term growth potential, making it one of the most attractive real estate investment opportunities in Africa today.

Looking to invest in high-growth markets like Nairobi? Explore opportunities with TwentyFirst Real Estate

Investor Implications And Opportunities

Core-Plus: Stabilised PBSA. Professionally managed, well-located PBSA assets with existing occupancy represent the closest equivalent to institutional-grade student housing in the market. Co-investment with established operators such as Qwetu, or direct acquisition of operational assets, is the primary access route. Due diligence should focus on lease roll, occupancy history across academic cycles, and operator covenant quality. Yields are more compressed than mid-market alternatives but more predictable.

Value-Add: Repositioning Under-Managed Stock. This is the most actionable strategy in the current window. Residential stock near major campuses along the Thika Road spine and inner corridors such as Ngara and Pangani is frequently informally managed, under-optimised for per-bed revenue, and available below replacement cost. Repositioning through structured leasing, utility upgrades, and bed reconfiguration can generate NOI uplift of 30 to 60 percent relative to pre-acquisition performance without expanding the building footprint. The repositioning cycle runs 6 to 18 months from acquisition to stabilised occupancy.

Development: Greenfield PBSA. Ground-up development is defensible in corridors where supply is genuinely scarce relative to institutional anchor strength, particularly around Kenyatta University’s catchment and select private university zones. The optimal profile is mid-rise and mid-specification, maximising bed count per floor plate while avoiding the full cost structure of premium PBSA. Development is most viable for investors with an existing land position, local construction capability, or an institutional pre-commitment.

Operational Platform. Building or acquiring a management and leasing business that operates third-party student housing assets is a capital-light entry point with strategic optionality. A credible operator with demonstrable track record and scalable systems can attract landlord mandates, build a portfolio under management, and create co-investment rights on preferential terms.

Portfolio Aggregation. The market’s fragmentation creates a consolidation opportunity. Acquiring multiple assets across one or two corridors under a single brand and management system builds income diversification and operational leverage, with an institutional exit as the medium-term value realisation event. South African operators including Respublica Student Living have demonstrated this model in a comparable emerging market context.

Capital and currency considerations. Local debt is available but expensive, and student housing does not yet attract specialist lender interest in Kenya. Investors with access to DFI capital from institutions such as the IFC,DEG, or British International Investment carry a structural financing advantage, particularly for assets with a demonstrable affordability component. Currency exposure should be underwritten in KES terms with any appreciation treated as upside rather than baseline return.

By Mitchell Wambui | Edited & published by TwentyFirst Real Estate.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or real estate advice. While we strive for accuracy, data and market conditions may change. Please consult a qualified professional before making any decisions.